Corporate Philanthropy

A corporate law and governance perspective

According to the Giving USA 2025 Report, donations to US charities hit a new record high in 2024, totalling $592.5 billion dollars. Over $44 billion of that total (7.5%) came from for-profit corporations, also a new record high. Total corporate profits that year totalled $4 trillion, yet another a record high, so corporate giving amounted to approximately 1.1% of corporate earnings. Not exactly tithing.

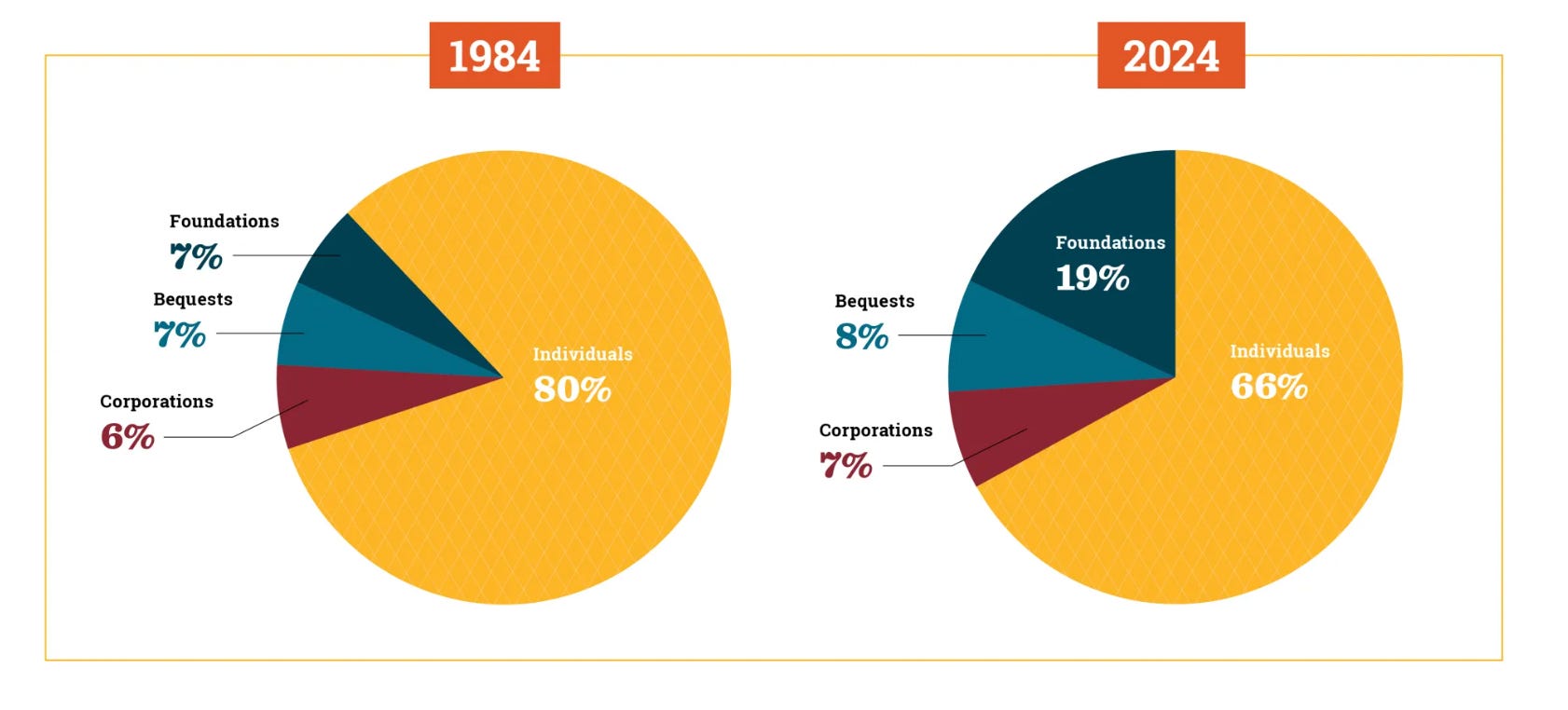

As a percentage matter, the share of corporate giving has remained roughly constant over the last 4 decades at 6-7%:

The forms corporate philanthropy takes varies from company to company, but the three most common are:

Corporate Grants & Sponsorships: Direct philanthropic contributions given to 501(c)(3) organizations or community foundations to support specific initiatives.

Employee Matching Gifts: The most common form of workplace giving, where companies match charitable donations made by their employees, often at a 1:1 ratio.

Volunteer Grants & Paid Time Off: Corporate programs that provide hourly grants to nonprofits where employees regularly volunteer.

Educational institutions tend to be the most common recipient of corporate gifts, with community funds (e.g., United Way), disaster relief, and health also being major recipient categories.

All of which raises two corporate law and governance questions:

Why do we care about corporate philanthropy?

What are the legal constraints on corporate philanthropy?

Should we strengthen the regulations on corporate giving?

Keep reading with a 7-day free trial

Subscribe to Bainbridge on Corporations to keep reading this post and get 7 days of free access to the full post archives.