The Appalling State of the Ordinary Business Grounds for Excluding a Shareholder Proposal

Rule 14a-8(i)(7) is not fit for purpose

A new opinion by Judge Leo Sorokin (D. Mass.), Dinapoli v. BJ’S Wholesale Club Holdings, Inc.,1 stands as a textbook example of why the SEC’s new policy of not issuing no action letters re shareholder proposals and why the Rule 14a-8(i)(7) ordinary business matters ground for excluding shareholder proposals from the issuer’s proxy statement is hopelessly muddled.

The discussion in this post draws in part on my article Stephen M. Bainbridge, Revitalizing SEC Rule 14a-8’s Ordinary Business Exclusion: Preventing Shareholder Micromanagement by Proposal, 85 Fordham L. Rev. 705 (2016), and in part on my book Corporate Law Concepts and Insights (5th edition 2025) (AMAZON LINK).

For a useful guide to the shareholder proposal rule, go here.

Plaintiff Thomas DiNapoli is the New York State Comptroller and, as such, Administrator of the New York State and Local Retirement System and Trustee of the New York State Common Retirement Fund (“Fund”).

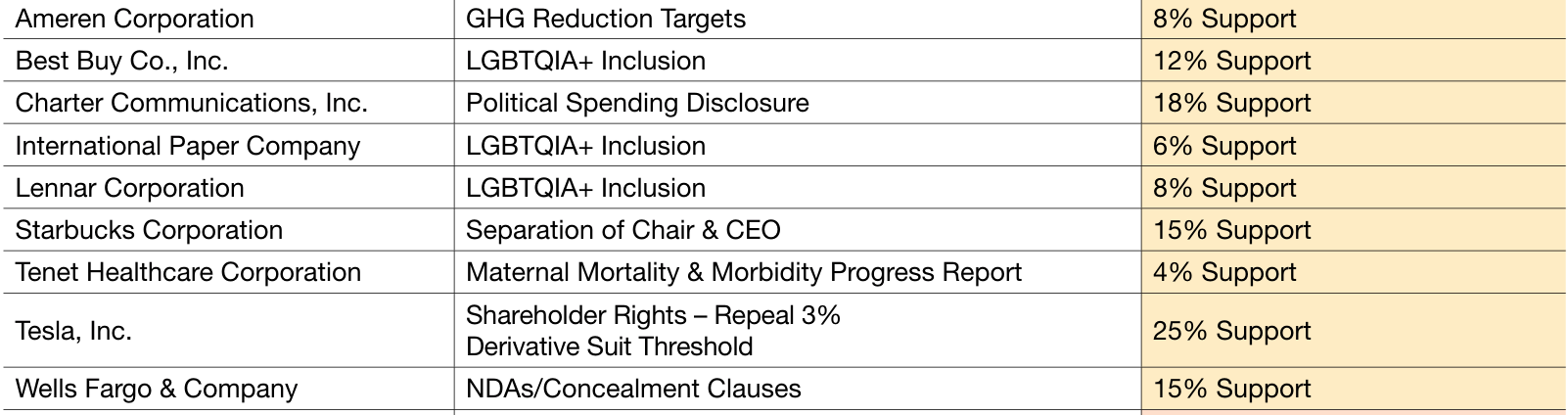

Along with the New York City Retirement System, the Fund is a very active player in the shareholder proposal game, having sponsored 30 proposals in 2024 and 17 in 2025. The vast majority of its proposals relate to social/political issues and environmental issues. Climate change is a major area of interest for the Fund as is DEI. The Fund’s proposals that make it to a shareholder vote rarely receive significant levels of support. In 2025, for example, 9 proposals made it to a vote. None got more than 25% of the vote:

In the present case, the Fund submitted an environmental proposal to BJ’s Wholesale Club:

RESOLVED: Shareholders request that BJ’s Wholesale Club Holdings, Inc. (“BJ’s” or “the Company”) conduct an assessment of risks of deforestation associated with its private-label brands within one year and provide a report summarizing the results. The report may, at management’s discretion, be updated annually and include an assessment of forest degradation within the supply chain; feasible, time-bound target setting; third-party monitoring and verification; and assessment of the financial and operational implications of the related risks.

Notice that the proposal is phrased as a request rather than as a mandate. This approach is driven by Rule 14a-8(i)(1), which provides that a proposal may be excluded from the company’s proxy statement if it relates to a matter that is not a proper subject of shareholder action. The SEC historically taken the position that such proposals must be excluded—assuming no other ground for exclusion exists—if they are phrased as a request or a recommendation.

As a mere request, the proposal is unlikely to have much of an impact on deforestation even if it passes.2 In addition to its status as a request, the proposal also gives BJ’s management essentially unbridled discretion, as Judge Sorokin pointed out:

All the granular considerations about how to conduct the assessment are left to BJ's discretion, including whether to assess the deforestation risks from a 40,000 foot view or on a microscopic level.

So why does the Fund bother? My theory is that the Fund and other ESG and corporate social responsibility proponents are driven by some combination of getting free advertising for their cause, performative virtue signalling, and a vague hope of shaming management into doing something about the subject of the proposal. Why the 75%+ of the shareholders who vote no on the Fund’s proposals should be required to pick up the tab for the Fund’s proposal remains something of a mystery.

It occurs to me that one useful reform would be to require shareholder proponents to reimburse the issuer for the costs associated with including the proposal in the proxy statement. Maybe having some skin in the game would lead to fewer and better proposals.

In any case, BJ’s announced that it would exclude the proposal from its 2026 proxy statement in reliance on the exemption provided by Rule 14a-8(i)(7) for ordinary business matters. The Fund sued, seeking an injunction requiring inclusion of the proposal. In a somewhat muddled opinion, Judge Sorokin granted the injunction.3

Keep reading with a 7-day free trial

Subscribe to Bainbridge on Corporations to keep reading this post and get 7 days of free access to the full post archives.